Duke v. Luxottica U.S. Holdings Corp., No. 24-3207, __ F.4th __, 2026 WL 303549 (2d Cir. Feb. 5, 2026) (Before Circuit Judges Robinson, Nathan, and Kahn)

This week’s notable decision, a published opinion from the Second Circuit, addresses a number of issues that often pop up in challenges to the administration of employee benefit plans, so rather than list them all up front, let’s just dive into the facts and see if you can spot them, law-school style.

The plaintiff was Janet Duke, a retired regional manager for Luxottica U.S. Holdings Corporation. Duke worked for Luxottica for nearly 21 years and was a participant in the Luxottica Group Pension Plan, a defined benefit plan.

On retirement, Duke had a choice of benefits. She selected the default option for married participants, a joint and survivor annuity (JSA) that would pay a percentage of her monthly benefit to her surviving spouse.

Under ERISA, a JSA has to be “actuarially equivalent” to a hypothetical single life annuity (SLA) that a participant would otherwise receive. In order to calculate Duke’s JSA, the plan’s benefits committee used a 7% annual interest rate and life expectancy values published in 1971. Duke contends that these assumptions were outdated, resulted in a benefit that was not actuarially equivalent to an SLA, and decreased her monthly benefit by about $54.

Duke filed this putative class action against her employer and related defendants, asserting four claims: violation of ERISA’s JSA equivalence requirement, violation of ERISA’s equivalence requirement for accrued benefits, violation of ERISA’s rules prohibiting forfeiture of retirement benefits, and breach of ERISA’s fiduciary duty obligations.

As for remedies, Duke sought “both reformation of the Plan to update its actuarial assumptions used to convert SLAs into JSAs, as well as monetary restitution to the Plan in the form of loss restoration and disgorgement of profits.”

Defendants moved to compel arbitration pursuant to Duke’s employment agreement, or, in the alternative, for lack of standing and failure to state a claim. The district court agreed with defendants that Duke lacked standing to pursue relief on behalf of the plan under ERISA Section 502(a)(2), and ruled that she must arbitrate her individual claims under Section 502(a)(3). (Your ERISA Watch covered this ruling in our October 11, 2023 edition.)

This decision was short-lived, however. The case was transferred, and the new judge granted plaintiffs’ motion for reconsideration. The court concluded that Duke had standing to assert a claim under Section 502(a)(2) on behalf of the plan for both reformation and monetary payments, and further ruled that the “effective vindication” doctrine precluded mandatory individual arbitration of that claim. The district court also denied defendants’ request to stay litigation of the claims under Section 502(a)(2) pending arbitration of the claims under Section 502(a)(3). (Your ERISA Watch covered this decision in our December 4, 2024 edition.)

Defendants filed interlocutory appeals from both the motion to compel arbitration and the motion to stay.

The Second Circuit began by discussing its own appellate jurisdiction. The court noted that it has the power to review certain interlocutory orders, including a district court’s denial of motions to compel arbitration and to stay litigation under the Federal Arbitration Act (FAA). However, here defendants were asking the court to review whether Duke had standing under Section 502(a)(2), which was “a determination of the district court’s subject matter jurisdiction that is not ordinarily immediately appealable.”

The court was not concerned, however. It ruled that the scope of an appealable order under the FAA “includes a district court’s determination that it has subject matter jurisdiction over the controversy to be litigated rather than stayed or arbitrated – including a plaintiff’s Article III standing.” Even if the scope was not this expansive, the Second Circuit ruled that it would consider the issue regardless as a matter of its pendent jurisdiction because standing and jurisdiction were “inextricably intertwined” with appealable issues.

The Second Circuit then turned to Duke’s Article III standing under Section 502(a)(2). The court divided this issue into two parts: whether Duke had standing to seek plan reformation, and whether Duke had standing to seek monetary payments to the plan.

On the first issue, defendants agreed that Duke’s receipt of decreased benefits was a “classic pocketbook injury” cognizable under Article III. However, they contended that plan reformation was a remedy “categorically unavailable under Section 502(a)(2) – which authorizes relief only to a plan – and thus Duke’s injury is not redressable under that provision.”

The Second Circuit was unconvinced, noting that defendants’ argument “targets the merits of Duke’s claims, not her standing to pursue them.” Furthermore, Duke was careful to argue that the harm to the plan was not her “receipt of reduced benefits,” but instead “its use of allegedly outdated actuarial assumptions,” which “renders the Plan in constant noncompliance with ERISA and jeopardizes its favorable tax status as a result.” Thus, while correcting that noncompliance would benefit Duke, that was not her point: “the Plan’s alleged noncompliance is its own injury that Duke seeks to remedy with Section 502(a)(2), rather than her receipt of decreased benefits, which is sufficient for standing[.]”

The court stressed that it was not reaching the issue of “whether ERISA noncompliance and attendant tax consequences really do constitute ‘plan injuries’ within Section 502(a)(2)’s remedial scope[.]” This was “an undecided question properly reserved for the merits.” Instead, the court merely held that Duke had standing to advance her arguments on the issue.

The Second Circuit reached a different conclusion as to Duke’s standing regarding monetary payments. Duke sought repayment of losses and disgorgement of profits to the plan, but defendants contended that only the plan would benefit from those remedies, not Duke, and thus she had no standing. Relying on the Supreme Court’s decision in Thole v. U.S. Bank, N.A., the court agreed with defendants.

Duke attempted to distinguish Thole with two arguments. First, she pointed out that the plaintiffs in Thole, unlike her, had received all their benefits. However, the Second Circuit responded that this did not matter because both plans were defined benefit plans. Thus, the plaintiffs in both cases “possessed ‘no equitable or property interest’ in the plan’s assets, and so monetary repayment to the plan would not benefit the plaintiffs personally.” Furthermore, Duke’s benefits were not reduced because of “a lack of Plan funds, but because of the Plan’s use of outdated actuarial assumptions.”

Duke’s second argument was that “the forms of relief she seeks will ‘work in tandem’ by increasing Plan funding commensurate with the reformation she hopes to obtain.” However, the court found that this argument was “foreclosed by Thole.” The court explained that the employer was the backstop for the plan, and thus was both “on the hook for plan shortfalls” and the recipient of any surplus after benefit payments. Thus, “nothing suggests monetary payments to the Plan will be necessary to effectuate any eventual reformation.” Either way, Duke “will be made whole regardless of whether the Plan receives additional funds; and if Duke is unsuccessful in seeking reformation, she will not be made whole regardless of whether the Plan receives those funds.” As a result, this claim “fails Article III’s redressability requirement.”

Next, the court considered arbitration. Duke contended that the effective vindication doctrine “precludes mandatory individual arbitration of her Section 502(a)(2) claim,” and the Second Circuit agreed. The court noted that it had already recognized the doctrine in the ERISA context in Cedeno v. Sassoon, and saw no reason not to apply it here.

Defendants offered three arguments against this conclusion, but the court rejected them, ruling that (1) Duke had properly alleged standing to bring her claim, as explained above, (2) it made no difference that this case involved a defined benefit plan, rather than a defined contribution plan as in Cedeno, because either way “only a representative action can resolve the allegedly detrimental effects of widespread violations of federal law,” and (3) defendants’ authorities regarding the scope of the FAA did not apply because Duke was not pursuing a “representative procedure” seeking “a personal remedy under Section 502(a)(2),” but was instead seeking relief on behalf of the plan for “a single absent principal.”

Finally, the Second Circuit addressed the district court’s denial of defendants’ motion to stay the litigation of Duke’s Section 502(a)(2) claim while the arbitration of her Section 502(a)(3) claim progressed. Defendants contended that a stay was mandatory under Section 3 of the FAA, but the court noted that “Section 3 does not extend to claims not subject to arbitration; whether a district court stays those is ‘a matter of its discretion to control its docket.’” The court observed that “Duke’s requested relief under Section 502(a)(2) is much broader than, and therefore not derivative of, her request under Section 502(a)(3).” Thus, the district court was within its discretion to allow the Section 502(a)(2) claim to continue.

As a result, Duke’s claims will proceed on two tracks: her Section 502(a)(3) claims in arbitration, and her Section 502(a)(2) claims in federal court. Of course, we’ll keep you updated on any further developments.

Below is a summary of this past week’s notable ERISA decisions by subject matter and jurisdiction.

Breach of Fiduciary Duty

First Circuit

Heet v. National Medical Care, Inc., No. CV 25-11644-WGY, __ F. Supp. 3d __, 2026 WL 353317 (D. Mass. Feb. 9, 2026) (Judge William G. Young). Plaintiffs Michelle Heet, Mike Bickle, Frank Luketich, and David Kitchell, participants in the Fresenius Medical Care North America 401(k) Savings Plan, brought this putative class action against National Medical Care, Inc. (d/b/a Fresenius Medical Care North America) and related defendants. Plaintiffs allege that defendants breached their fiduciary duties under ERISA by improperly applying forfeited matching contributions. According to the plan, these forfeited contributions should be used to reduce company contributions and offset administrative expenses. However, plaintiffs allege that from 2019 through 2024, the defendants applied these forfeitures only to reduce matching contributions and not to administrative expenses. Defendants moved to dismiss. The court noted, and readers of Your ERISA Watch are well aware, that this is a hot topic in ERISA litigation. The court explained, “There are two schools of thought here. On the one hand, fiduciaries typically argue that they are not required to maximize benefits, only to ensure that the benefits due plan participants are appropriately disbursed. Accordingly, the reallocation of forfeited benefits to other matching contributions due as opposed to paying off administrative expenses is appropriate. On the other hand, plan participants typically argue that fiduciaries are conflicted when presented with a choice about using forfeited contributions to pay down matching contributions due from the company and thereby benefit the coffers of the company, as opposed to paying down administrative expenses to plan beneficiaries.” The court characterized this as “a zero-sum game: using chargeable forfeited matching contributions to defray other contributions due from the company obviously benefits the company, while administrative expense defrayment benefits the plan participants.” The court noted there was no controlling ruling from the First Circuit on the issue, or a ruling by any Circuit for that matter. It observed that the majority of courts have ruled against plaintiffs, but “[h]ere, this Court follows persuasive authority adopting the minority position.” Addressing plaintiffs’ specific claims, the court ruled against plaintiffs on their first count for failure to follow plan terms. The court ruled that the plan was “unambiguous” in that it “requires forfeited matching contributions to be used to offset other matching contributions…and, once those are paid, the only other permissible, albeit discretionary, use under the Fresenius Plan expands to defrayment of administrative expenses[.]” However, this ruling did not compel the court to find for defendants on plaintiffs’ other claims because “ERISA’s statutorily imposed fiduciary duty of prudence ‘trumps the instructions of a plan document.’” On plaintiffs’ claims for breach of the duties of loyalty and prudence the court found that plaintiffs did not allege overbroadly that forfeitures must always be used to pay expenses. Instead, they alleged, sufficiently for the court, that defendants failed to act solely in the interest of plan participants in making their decisions and did not adequately investigate the best use of forfeited contributions. In this way the court distinguished its ruling from others, such as Hutchins v. HP, which had granted motions to dismiss. As for plaintiffs’ prohibited transactions claim, the court granted defendants’ motion, ruling that the reallocation of forfeitures did not qualify under the statute. Finally, the court denied defendants’ motion as to plaintiffs’ failure to monitor claim to the extent it was dependent on plaintiffs’ other claims that survived. As a result, the split deepens among the district courts on this issue.

Sixth Circuit

Sweeney v. Nationwide Mut. Ins. Co., No. 2:20-CV-1569, 2026 WL 352845 (S.D. Ohio Feb. 9, 2026) (Judge Sarah D. Morrison). This is a certified class action by former employees of Nationwide Mutual Insurance Company who were participants in the company’s 401(k) plan, the Nationwide Savings Plan. They claim that Nationwide Mutual, Nationwide Life Insurance Company, and members of the Plan’s Benefits Investment Committee (BIC) violated ERISA by maintaining the Guaranteed Fund (“a stable value investment vehicle backed by a Nationwide Life annuity contract”) as an investment option for plan participants. The Guaranteed Fund “is a heavily utilized investment option for Plan Participants. As of 2020, 86% of Plan Participants had some portion of their account invested in the Guaranteed Fund, accounting for $1.75 billion.” The plan also had several features that encouraged investment in the Fund, including a target date fund which included the Fund as a portfolio component, and an “easy enroll” option for new participants which automatically invested them in the Fund. Plaintiffs contend that the BIC’s mismanagement led to the plan overpaying for the Fund, benefiting Nationwide at the expense of plan participants. They alleged several claims under ERISA, including breach of fiduciary duty, prohibited transactions, self-dealing, and anti-inurement. Before the court here were several pre-trial matters, including cross-motions for summary judgment and expert-related motions. The court addressed the expert motions first, denying defendants’ motion to exclude because plaintiffs’ two experts were qualified and their opinions were helpful and relevant. The court granted plaintiffs’ motion to exclude in small part, ruling that defendants’ financial analyst could not testify as to legal conclusions (such as “whether the Annuity Contract is a prohibited transaction”). The court then turned to the summary judgment motions. Defendants asserted two “safe harbors” in its motion: ERISA Section 408(b)(5)’s exemption and the “transition policy” safe harbor. The court ruled that summary judgment was not appropriate on this issue because genuine disputes of material fact existed. Under Section 408(b)(5), there were questions as to whether the plan paid “no more than adequate consideration” and whether the process that led to the annuity contract price complied with defendants’ fiduciary duties. For similar reasons, the court found that defendants failed to establish that the annuity contract qualified as a transition policy. Turning to the merits of plaintiffs’ claims, the court found that there was a genuine dispute of material fact as to whether the BIC fulfilled its fiduciary duties in overseeing Fund expenses. The court also found that there were factual questions regarding whether the plan, investment policy statement, and annuity contract were monitored and followed. As for plaintiffs’ claims for prohibited transactions and self-dealing, the court ruled that genuine disputes of material fact prevented a finding that Section 408(b)(5) applied as a defense to these counts. The court also found that the statute of repose does not bar these claims to the extent they are based on rate setting within the six-year period before Plaintiffs filed suit. Under plaintiffs’ claim for self-inurement, the court granted defendants’ motion to the extent the claim was based on conduct outside the six-year period before plaintiffs filed suit. Finally, the court considered named plaintiff Bryan Marshall, whom defendants contend released any ERISA claims he had. However, the court found that Marshall’s release did not affect his ability to bring a claim on behalf of the plan, as such claims belong to the plan. As a result, most of the relief sought by both sides was denied, and this case will proceed to a bench trial.

Seventh Circuit

Russell v. Illinois Tool Works, Inc., No. 22 CV 02492, 2026 WL 332662 (N.D. Ill. Feb. 9, 2026) (Judge Sunil R. Harjani). Employees of Illinois Tool Works, Inc. (ITW) brought this action in 2022 alleging that ITW and related defendants violated ERISA by breaching their duties of prudence and monitoring in mismanaging the company’s retirement plan. Defendants filed a motion to dismiss which the court denied in 2024, ruling that plaintiffs’ allegations were similar enough to the allegations in Hughes v. Northwestern University, which the Seventh Circuit had deemed sufficient. In 2025, plaintiffs filed a motion to amend their complaint to add allegations regarding defendants’ use of plan forfeitures. In their new allegations plaintiffs contend that defendants allocated unvested benefits, which had been forfeited back to the plan, to reduce ITW’s contributions rather than plan expenses borne by participants. Defendants moved to dismiss. The court first addressed defendants’ statute of limitations argument. The court determined that plaintiffs’ new claims did not relate back to the original 2022 complaint because they were based on new factual allegations regarding the use of forfeitures, which were not included in the original complaint. As a result, any claims related to conduct before February 21, 2019, were barred by ERISA’s six-year statute of limitations. On the breach of fiduciary duty claim, the court ruled that plaintiffs sufficiently alleged that defendants acted as fiduciaries, and not as plan settlors, with regard to their use of the forfeitures. The court noted two potentially conflicting plan provisions and held that “[a] reasonable reading that gives effect to both provisions is that some forfeitures in a given year must be used to reduce employer contributions, but not necessarily all. Under this interpretation, Defendants would retain discretion to allocate the remainder to further reduce employer contributions or reduce Plan expenses.” As a result, it was “reasonable” for plaintiffs to allege that the plan granted defendants discretion, and thus reasonable to allege that defendants were acting in a fiduciary capacity. The court further held that plaintiffs’ claim survived because they did not allege a “per se ban on the use of forfeitures for reducing employer contributions.” Instead, “Plaintiffs assert that Defendants breached their duties by not considering whether specific forfeiture allocations benefited the Plan participants rather than just themselves and choosing the option that only benefited themselves.” For similar reasons, the court ruled that plaintiffs could pursue their duty of loyalty claim. The court reiterated that plaintiffs were not seeking a per se rule and “only allege liability for certain forfeiture use under the circumstances presented here.” Defendants argued that the plan and government regulations authorized them to allocate the forfeitures as they did, but “[t]he mere fact that Defendants can make these allocations under the Plan is not mutually exclusive with the allegation that they were motivated by selfish purposes that breached their duty of loyalty. Further, the Court cannot create a presumption of loyalty based on a plan’s allowance of an action because ERISA’s duties ‘trump[] the instructions of a plan document.’” The court further ruled that there was harm to the plan, because expenses paid by plaintiffs left the plan, and that plaintiffs plausibly pled an anti-inurement violation because the benefit to defendants was not “incidental,” but instead “a direct benefit that motivated their actions.” The court also upheld its earlier ruling that plaintiffs had adequately pled a breach of the duty of monitoring against ITW and its board. However, the court dismissed plaintiffs’ co-fiduciary liability claim against the plan’s investment committee because “Plaintiffs do not allege how a breach by the Committee enabled a breach by ITW or the Board.” As a result, defendants’ motion was granted in part, but denied on the issues that mattered most: “Plaintiffs have sufficiently alleged that Defendants acted as fiduciaries, used forfeitures to reduce employer contributions instead of Plan expenses in violation of ERISA’s fiduciary duty of loyalty and anti-inurement provision, and harmed Plaintiffs through a loss of benefits.”

Eighth Circuit

Plesha v. Ascension Health Alliance, No. 4:24-CV-01459-CMS, 2026 WL 279321 (E.D. Mo. Feb. 3, 2026) (Judge Cristian M. Stevens). In this putative class action Jennifer L. Plesha challenges the tobacco surcharge provision in the ERISA-governed health benefit plan administered by her employer, Ascension Health Alliance. Under the plan, “any member who used tobacco products in the past three years was required to identify himself as a tobacco user during enrollment for the next year… Tobacco users were surcharged an additional $750 per year, or about $30 per paycheck.” However, tobacco users could avoid this surcharge by participating in a wellness program, which qualifies as a “reasonable alternative standard” under ERISA. Plesha paid the surcharge, and now brings three claims for relief. First, she claims that the plan violates ERISA, specifically 29 U.S.C. § 1182(b), because it does not provide the “full reward” for participating in the wellness program. Specifically, she contends that the plan does not provide a refund for the entire year if a participant completes the program. Second, she claims that Ascension “failed to provide the required notice of a reasonable alternative standard that would allow participants to avoid paying the tobacco surcharge for the entire plan year, as required by applicable regulations.” Third, she contends that Ascension breached its fiduciary duty by assessing the surcharge. Ascension filed a motion to dismiss. On Plesha’s first count, Ascension contended that “full reward” in the statute meant only that it had to remove the surcharge prospectively, not retroactively, and the court agreed. “Nothing in the text…suggests that that particular reward must be given retroactively, and Congress knew how to mandate retroactive reimbursement when it enacted the PHSA.” The court also stated that Plesha’s interpretation would “frustrate Congress’ stated purpose in creating the wellness program scheme” because withholding retroactive reimbursement would incentivize insureds to participate in the plan sooner. Plesha asked the court to “defer to the regulatory definition of ‘full reward’ found in the 2013 preamble” to the Department of Labor’s interpreting regulations, but the court declined because the statute was unambiguous, could not be overridden by regulation, and the court was not obligated to show the preamble or the regulations any special deference. (For a contrary view, see last week’s edition in which we summarized the court’s decision in Wilson v. Whole Food Market, Inc. that “to make available the ‘full reward’ to ‘all similarly situated individuals,’ a wellness program must provide retroactive reimbursements of all tobacco surcharges paid that Plan year.”) As for Plesha’s second claim, the court ruled that Plesha lacked Article III standing. The court determined that Plesha’s alleged injuries – not receiving proper notification – were “purely informational” and did not satisfy the concreteness requirement for standing. Plesha also did not allege how her behavior would have changed if she had received proper notice: “Put another way, Plaintiff would be in the exact same place with or without the purported defects in the notice.” Plesha’s third count met the same fate as the first two. The court agreed with Ascension that it did not breach any fiduciary duty because the plan complied with ERISA. The court also found that Ascension acted as a settlor, not a fiduciary, in creating and administering the plan. As a result, the court granted Ascension’s motion to dismiss in its entirety and dismissed the case with prejudice.

Ninth Circuit

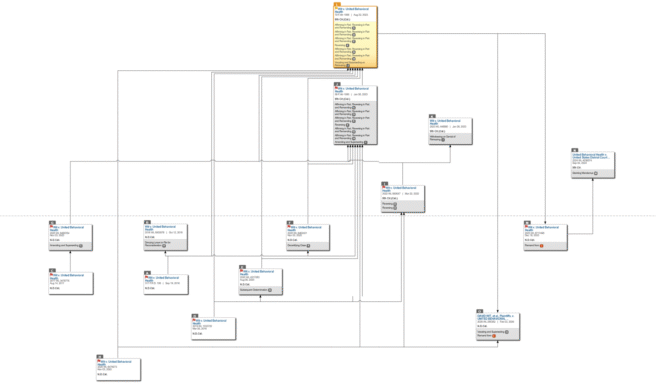

Wit v. United Behavioral Health, No. 14-CV-02346-JCS, 2026 WL 290352 (N.D. Cal. Feb. 3, 2026) (Magistrate Judge Joseph C. Spero). This class action, originally filed in 2014, has a long and tortured history, including numerous Ninth Circuit rulings. (We covered the Circuit’s published 2023 decision as our case of the week in our August 30, 2023 edition.) The Westlaw history map says it all:

The decisions above the dotted line are from the Ninth Circuit. In the course of issuing those decisions, the Ninth Circuit significantly scaled back the district court’s extensive rulings against United Behavioral Health in which the district court found that UBH breached its fiduciary duty to health plan participants in its misuse of mental health guidelines to deny patient claims. The Ninth Circuit’s rulings left several issues open, however, and the district court tried to sort it all out in an August 5, 2025 order, as we explained in our August 13, 2025 edition. In that order the court acknowledged that the Ninth Circuit had eliminated parts of the plaintiffs’ breach of fiduciary duty claim, but ruled that other parts survived: “the Court’s findings as to the breach of the duty of care and the duty of loyalty are not intertwined with the erroneous interpretation of the Plans identified by the [Ninth Circuit] Panel and therefore, the Court’s judgment on the breach of fiduciary duty claim survives to the extent that it is based on those theories.” The district court further ruled that the fiduciary duty claim was not subject to exhaustion requirements, and even if it were, exhaustion would be excused as futile because of UBH’s uniform application of its guidelines. The court ordered the parties to meet and confer, and after further submissions, it issued this judgment. The court declared that UBH acted as a fiduciary under ERISA when it developed level of care guidelines and coverage determination guidelines for making coverage determinations, which were not terms of the class members’ plans. Those plans required services to be consistent with generally accepted standards of care (GASC), and UBH’s guidelines were used to interpret this requirement. However, although the class members “had a right, under ERISA and their plans, to have UBH adopt Guidelines that were developed solely in the interests of the class members and with care, skill, prudence, and diligence,” they “were deprived of this right” because the guidelines were “tainted by UBH’s financial interests and its lack of due care.” Furthermore, “UBH’s misconduct in developing and adopting its Guidelines was willful and systematic,” “affected the class members across-the-board,” and violated ERISA’s statutorily imposed duties of loyalty and care. The court noted that UBH’s guidelines “purport to be based on generally accepted standards of care.” However, the court compared the guidelines to the standards that “are generally accepted in the field of mental health and substance use disorder treatment and patient placement,” and concluded that UBH’s guidelines in fact “do not accurately reflect generally accepted standards of care. They are instead significantly and pervasively more restrictive than those standards. This defect is a direct result of UBH’s self-interest and lack of due care[.]” Among other failures, the court noted that UBH’s guidelines inappropriately emphasized acuity and crisis stabilization over effective treatment of underlying conditions, failed to address co-occurring conditions, did not address the unique needs of children and adolescents, and did not err on the side of caution for higher levels of care. The court further found that “UBH affirmatively misled regulators about its Guidelines” and violated the laws of Connecticut, Illinois, Rhode Island, and Texas in applying its too-strict guidelines. As a result, the court ruled that UBH “breached its fiduciary duties to the class members, including its obligations under 29 U.S.C. §§ 1104(a)(1)(A), and (a)(1)(B), when it developed, revised, and adopted the Guidelines.” The court imposed injunctive relief, (1) permanently enjoining UBH from using the invalidated guidelines to implement the GASC requirement in ERISA-governed plans, and (2) ordering UBH, in adopting criteria to interpret ERISA-related plans, to ensure that its criteria “accurately reflect GASC” and comply with state law. The second requirement will be in effect for the next five years, during which the court will maintain jurisdiction. Will UBH once again appeal to the Ninth Circuit? Given the history of this case, it would be astonishing if it did not. Either way, we will let you know of any further developments.

Class Actions

Sixth Circuit

Best v. James, No. 3:20-CV-299-RGJ, 2026 WL 357964 (W.D. Ky. Feb. 9, 2026) (Judge Rebecca Grady Jennings). In a case with one of the shortest names we have had the pleasure of covering here at Your ERISA Watch, plaintiffs Nathan Best, Matthew Chmielewski, and Jay Hicks have sued defendants ISCO Industries, Inc., James Kirchdorfer, and Mark Kirchdorfer. Plaintiffs have alleged various ERISA claims against defendants, including fiduciary breach and engaging in a prohibited transaction in connection with ISCO’s Employee Stock Ownership Plan (“ESOP”). In 2022, the court granted defendants’ motion to compel arbitration, and in 2023 it denied plaintiffs’ motion for reconsideration, in which plaintiffs argued that the effective vindication doctrine invalidated the operative arbitration provision. However, in 2024 the Sixth Circuit decided Parker v. Tenneco, in which it applied the effective vindication doctrine to strike down an arbitration provision similar to the one in this case. Based on Parker, plaintiffs filed another motion for reconsideration, and in 2025 the court granted it, agreeing that Parker was a change in controlling law that required it to vacate its prior order. Plaintiffs then filed a motion for class certification, seeking to certify a class of all persons who were participants in the ISCO ESOP when it sold its shares in 2018. The motion was unopposed and granted by the court in this order. The court marched through the Federal Rule of Civil Procedure 23(a) requirements: numerosity, commonality, typicality, and adequacy of representation. The proposed class consisted of over 400 participants, satisfying the numerosity requirement. Commonality was met as the case involved common questions of law and fact, such as whether the defendants breached fiduciary duties under ERISA. Typicality was satisfied because the plaintiffs’ claims arose from the same conduct affecting all class members. Adequacy of representation was confirmed as the plaintiffs had common interests with the class and were represented by qualified counsel. The court also considered Rule 23(b) requirements, determining that certification was appropriate under Rule 23(b)(1)(B) because the case involved ERISA fiduciary duty claims, which typically require plan-wide relief. This subsection was deemed suitable because adjudications for individual class members could affect the interests of others not party to the adjudications. Finally, under Rule 23(g), the court appointed Kaplan Johnson Abate & Bird LLP as class counsel, finding them qualified based on their experience and the work done in the case.

Disability Benefit Claims

Eighth Circuit

Jackson v. The Hartford Financial Servs. Grp., Inc., No. 4:25-CV-01329-JAR, 2026 WL 352912 (E.D. Mo. Feb. 9, 2026) (Judge John A. Ross). Lynette Jackson, a former employee of American Water, asserts that she filed a claim for disability benefits with The Hartford Financial Services Group in 2019 due to unspecified health conditions. She brought this pro se complaint against Hartford accusing it of bad faith and fraudulent practices, including underpaying her short-term disability benefits and incorrectly asserting that she lacked long-term disability coverage. Jackson alleged that these actions led to her termination from American Water in 2020, resulting in severe financial hardship and emotional distress. She seeks $300 million(!) in compensatory and punitive damages. Jackson brought claims under several state and federal laws, including ERISA, the Americans with Disabilities Act (ADA), the Rehabilitation Act, and the Family and Medical Leave Act (FMLA). Jackson filed a motion for leave to proceed in forma pauperis, the appointment of counsel, leave to amend, and to compel a ruling. The court quickly dismissed Jackson’s state law claims, ruling that because they “arise directly from the administration of her employee health plan, they are preempted” by ERISA. As for Jackson’s ERISA claims, the court ruled that “Jackson does not identify a particular disability, impairment, or medical condition, nor does she allege any facts describing functional limitations that would bring her condition within the plan’s definition of disability… Jackson’s allegation that she became ‘medically unable to work’…is a ‘naked assertion’ devoid of ‘further factual enhancement.’” This was insufficient under federal pleading standards and thus the court dismissed her ERISA claims. The court also dismissed Jackson’s other claims, ruling that (1) under the ADA and Rehabilitation Act she did not sue her former employer, American Water, but rather Hartford, and did not allege that Hartford discriminated against her based on her disability, and (2) under the FMLA she again did not allege that Hartford was her employer, which was necessary to establish a violation under the FMLA. As for Jackson’s motion to amend, the court determined that her proposed amendment would be futile because it did not address the deficiencies in her original claims or establish a new cause of action against Hartford. As a result, the court granted Jackson’s motion to proceed in forma pauperis but dismissed the action without prejudice for failing to state a plausible claim for relief.

Medical Benefit Claims

Second Circuit

Savage v. Rabobank Med. Plan, No. 24-2759-CV, __ F. App’x __, 2026 WL 303600 (2d Cir. Feb. 5, 2026) (Before Circuit Judges Calabresi, Raggi, and Lee). The plaintiff in this case is Sheri Savage, who is the executor of the estate of Cindy Sieden. The case revolves around Sieden’s daughter, J.S., who suffered from a severe eating disorder and mental health conditions. J.S. had been receiving treatment for her eating disorder since she was eight years old, including residential treatment and partial hospitalization. In 2016 J.S. was admitted to Avalon Hills Adolescent Treatment Facility. Sieden submitted claims for J.S.’ treatment at Avalon to United Behavioral Health (UBH), the mental health claims administrator for the Rabobank Medical Plan, under which J.S. was a covered dependent. Initially, UBH approved her claims, but as of February 2017, UBH determined that J.S. no longer met the criteria for partial hospitalization or residential care and denied further coverage. Appeals were unsuccessful, and UBH did not respond to post-service claims from Avalon, so Savage brought this action. On cross-motions for summary judgment, the district court applied an arbitrary and capricious standard of review because the plan conferred discretion on UBH. The court affirmed UBH’s use of its level of care guidelines and held that Avalon’s post-service submission functioned as an additional appeal rather than a new claim requiring a merits determination, thus not altering the standard of review. The court ultimately ruled that UBH’s denials were not an abuse of discretion. (Your ERISA Watch covered this ruling in our October 9, 2024 edition.) Savage appealed to the Second Circuit, which issued this unpublished opinion. On appeal, Savage argued that (1) the district court was bound by findings made in Wit v. United Behavioral Health regarding UBH’s level of care guidelines (see above for the latest installment in the Wit case), (2) UBH’s denials were arbitrary and capricious, and (3) Avalon’s post-service claims were subject to de novo review and were supported by unrebutted medical evidence. The Second Circuit rejected all three arguments. First, the court ruled that the collateral estoppel argument regarding Wit was forfeited because it was not raised in the district court; instead, Savage had used the Wit ruling “more generally as persuasive authority.” Furthermore, the Second Circuit noted that the Ninth Circuit in Wit did not require UBH’s level of care guidelines to be coextensive with generally accepted standards of care. As for the denial of benefits, the court acknowledged there was evidence in support of both sides as to the medical necessity of J.S.’ treatment. However, “[g]iven the substantial deference afforded to ERISA administrators, the record here does not overcome the requisite standard to warrant overturning the denial of benefits.” Finally, the Second Circuit rejected Savage’s arguments regarding the post-service claim, noting that “voluntary appeals” are not subject to “ERISA safeguards” and thus the claim did not require de novo review. The court further stated that the “post-service submission appears to largely repackage claims for services that had already been denied with overlapping dates.” As a result, the court upheld the district court’s rulings on the post-service submission as well, and affirmed the judgment below. (Disclosure: Kantor & Kantor represented Ms. Savage in this action.)

Seventh Circuit

R.S. v. Quartz Health Benefit Plans Corp., No. 22-CV-418-WMC, 2026 WL 309629 (W.D. Wis. Feb. 5, 2026) (Judge William M. Conley). Plaintiff R.S. was a participant in an employee health benefit plan insured and administered by Quartz Health Benefit Plans, and his son, A.S., was a covered dependent under the same plan. A.S. has a history of behavioral and mental health difficulties from an early age, including diagnoses of attention deficit hyperactivity disorder and “extreme” oppositional defiant disorder. A.S. was failing his school classes, had suicidal thoughts, used drugs, and stole from his parents. “When confronted, A.S. also attacked his father, destroyed parts of his car, and threatened to have his friends kill him.” A.S.’ therapist recommended inpatient treatment, so A.S. was admitted to Triumph Youth Services, a residential mental health facility in Utah. Quartz initially covered A.S.’ treatment at Triumph for 34 days but later denied further coverage, stating that continued residential treatment was not medically necessary. Appeals were unsuccessful, so R.S. filed this action, alleging that Quartz violated ERISA by denying coverage for A.S.’ treatment, and violated the Mental Health Parity and Addiction Equity Act. The parties filed cross-motions for summary judgment. R.S. acknowledged that the benefit plan gave Quartz discretionary authority to make benefit determinations, but argued that because of Quartz’s procedural violations, it had forfeited any deference. The court decided it “need not resolve this dispute because, as discussed below, defendant’s decision denying benefits was arbitrary and capricious under even the more deferential standard.” The court found that Quartz did not provide a full and fair review because it did not give its medical review report to R.S. until litigation, even though ERISA’s claim procedure regulation required it to do so before denying the appeal. The court further ruled that Quartz erred by failing to consider A.S.’ severe substance abuse disorder. Quartz never addressed his substance abuse in any of its reports or denials, and “[g]iven its length and comorbidity, defendant’s failure to address plaintiff’s substance abuse disorder as powerful evidence supporting his need for ongoing, residential treatment was arbitrary and capricious.” The court rejected Quartz’s contentions that (1) A.S.’s substance abuse was not a focus of his treatment, finding that this was belied by the record, and (2) Quartz considered the substance abuse by implication even if it never directly discussed it. “[A] vague reference that all records were reviewed is not sufficient under the circumstances here, in which plaintiff asked specifically and repeatedly that defendant consider his substance abuse treatment needs on appeal, just as his primary care providers did at Triumph.” The court thus granted R.S.’ motion, and remanded the case to Quartz for further findings and explanations. R.S. had less luck with his Parity Act claim. R.S. contended that the plan violated the Parity Act because it required “acute” symptomatology for mental health coverage while the analogous skilled nursing plan provisions did not. The court seemed sympathetic to the argument; a comparison “appears to support plaintiff’s assertion.” However, the court ruled that the claim, as presented, was “poorly developed” and that R.S. did not address several of Quartz’s arguments in opposition. As a result, the court denied R.S.’ motion as to his Parity Act claim. However, the court stated that on remand Quartz “should consider whether its review of plaintiff’s claim satisfies the concerns raised by the court and plaintiff under the Parity Act, as the court’s decision is not intended to foreclose plaintiffs from raising a new as-applied challenge under the Parity Act to a new decision by defendant.”

Pension Benefit Claims

Second Circuit

Dimps-Hall v. Employee Benefit Plan Administration Committee HSBC-North America, No. 25-CV-00421 (LJL), 2026 WL 305485 (S.D.N.Y. Feb. 5, 2026) (Judge Lewis J. Liman). In this action Shirley A. Dimps-Hall seeks benefits under the Manhattan Savings Bank (MSB) pension plan. She alleges that a temporary agency placed her at MSB in 1982, but she was hired as a full-time employee by MSB in 1983, and was a permanent employee of MSB from that year until April of 1991, when she retired as Senior Bookkeeper. Before she retired, MSB was taken over by Republic National Bank of New York. Republic was, in turn, acquired by HSBC in 1999. In 2023, Dimps-Hall submitted a claim contending she was entitled to pension benefits beginning in 2019, when she turned 65, pursuant to her employment at MSB and Republic. HSBC denied her claim. HSBC stated that under the Republic pension plan, which was in effect at the time of Dimps-Hall’s retirement, participants were eligible for benefits if they had “completed at least 5 RNB Years of Service.” Active participants in the MSB plan when MSB was taken over by Republic were given credit for their employment at MSB. However, “HSBC’s records, including IRS Employee Census Reports for the Retirement Plan of the Manhattan Savings Bank…from 1988, 1989 and 1990, reflect that you were first hired by MSB on July 20, 1987.” As a result, HSBC told Dimps-Hall that she did not have five years of vesting service when she retired in 1991, and was not eligible for benefits. Dimps-Hall unsuccessfully appealed this decision and then filed this pro se action against HSBC. HSBC moved to dismiss. The court noted that the plan gave HSBC discretionary authority to determine eligibility for benefits, and thus the arbitrary and capricious standard of review applied. The court agreed with HSBC that it was appropriate for HSBC to rely on its records in denying Dimps-Hall’s claim because such reliance “promotes uniformity, predictability, and efficiency. Those features, in turn, protect all participants as a group. They help ensure that benefits are calculated according to the same rules for everyone, that the Plan can be funded and administered at a reasonable cost, and that assets are reserved for the benefits promised under the Plan rather than spent on repeated reconstruction of decades-old employment histories whenever a dispute arises.” Thus, “It is not enough to allege that other records might exist somewhere, or that further searching might yield a different picture.” As a result, the court ruled that Dimps-Hall had not plausibly pled that HSBC abused its discretion. HSBC had relied on its records in making the decision, and “[t]he fact that Plaintiff believes those records to be incomplete, or believes that other documents might exist that would support her view of her employment history, does not by itself render the Committee’s decision arbitrary and capricious, particularly where the Plan expressly permits the Committee to ‘conclusively rely’ on those records.” The court further rejected Dimps-Hall’s contention that she should be allowed to conduct discovery to find supporting evidence of her employment, noting that discovery beyond the administrative record is typically not allowed. Furthermore, because the plan allowed HSBC to “conclusively rely” on its records, “even if there existed documents in the bowels of the bank that would tend to show that Plaintiff was a full-time, salaried employee prior to 1987, that would not make the Committee’s decision arbitrary and capricious.” The court then quickly disposed of Dimps-Hall’s remaining claims, ruling that (1) she was not a plan participant and thus could not sue for statutory penalties, and in any event HSBC responded appropriately to her inquiries, (2) her breach of fiduciary duty claim was duplicative of her claim for benefits, and (3) she did not have a private right of action to sue for violations of Department of Labor regulations. The court further struck her jury demand as there is no right to a jury trial in ERISA benefit actions. The court thus granted HSBC’s motion in full, and dismissed Dimps-Hall’s complaint with prejudice, ruling that it would be futile to allow her to amend.

Sixth Circuit

Alliance Coal, LLC v. Smith, No. 0:26-CV-10-REW-EBA, 2026 WL 353029 (E.D. Ky. Feb. 9, 2026) (Judge Robert E. Wier). This is an interpleader action initiated by Alliance Coal, LLC, concerning the distribution of retirement plan benefits following the death of Constance Smith, a long-time employee of Excel Mining, LLC, a subsidiary of Alliance Coal. In 2007 Constance designated Dusty L. McCoy, her second cousin, as the primary beneficiary of her account in Alliance Coal’s 401(k) retirement plan, which was managed by INTRUST Bank. After Constance’s death in December 2024, her brother, Larry Smith, contested this designation, presenting a beneficiary form dated February 21, 2024, which allegedly named him as the sole beneficiary. Larry claimed that Constance did not file this form due to misrepresentations by INTRUST Bank representatives, who allegedly told her that she did not need to update her beneficiary designation. Alliance Coal thus filed this action to allow the court to determine who was the proper beneficiary. Larry responded by filing counterclaims against Alliance Coal and McCoy, alleging breach of fiduciary duty, equitable estoppel, reformation of plan documents, and breach of plan requirements under ERISA. McCoy and Alliance Coal filed motions to dismiss. Addressing the Alliance Coal motion first, the court held that Larry could not obtain individual relief under ERISA § 502(a)(2) because his claims did not benefit the plan as a whole. Additionally, his claims under ERISA § 502(a)(3) failed because he did not adequately allege that Alliance Coal made any misrepresentations, or that INTRUST Bank’s actions could be attributed to Alliance Coal. (The court noted that INTRUST Bank, although named by Larry as a counter-defendant, had not appeared in the case and Larry conceded that INTRUST Bank was not a target of his claims.) Furthermore, Larry could not bring a breach of plan requirements claim under ERISA § 502(a)(1)(B) because he “does not identify a plan provision entitling him to the disputed benefits… Rather, he argues that he should be entitled to the disputed benefits on account of Ms. Smith’s intent and the communications history… He fails to highlight any plan provision that Alliance Coal itself has broken[.]” The court further ruled that Larry could not pursue a surcharge remedy because of Sixth Circuit precedent, and was not entitled to a jury trial. Thus, the court granted Alliance Coal’s motion in its entirety, with prejudice. This ruling rendered McCoy’s motion to dismiss moot, so the court did not discuss it in any detail, other than to note that Larry’s counterclaims did not allege any facts supporting a claim against her, and were primarily directed at Alliance Coal. The dismissal was with prejudice.

Pleading Issues & Procedure

Second Circuit

Sacerdote v. Cammack Larhette Advisors, LLC, No. 17-CV-8834 (AT) (VF), 2026 WL 350842 (S.D.N.Y. Feb. 9, 2026) (Magistrate Judge Valerie Figueredo). This is a long-running action in which employees of New York University allege that Cammack Larhette Advisors, LLC, the investment advisor to the plans, breached its fiduciary duty by providing imprudent advice, resulting in substantial losses to the plans. (The Second Circuit’s ruling reviving this case was the notable decision in our October 8, 2019 edition.) Before the court here was plaintiffs’ motion to join CapFinancial Group, LLC as a party under Federal Rule of Civil Procedure 25(c). “Plaintiffs contend that Cammack transferred its assets, operations, and personnel to CapTrust following an acquisition that occurred in February 2021… More specifically, Plaintiffs argue that CapTrust is the successor-in-interest to Cammack because it substantially continued Cammack’s business operations, personnel, and client relationships, and CapTrust had actual or constructive notice of Plaintiffs’ claims against Cammack at the time of the acquisition.” CapTrust opposed plaintiffs’ motion, arguing it was untimely under the court’s scheduling order, and thus plaintiffs had to show “good cause” to amend under Federal Rule of Civil Procedure 16. CapTrust also argued that ERISA forecloses successor liability for breaches of fiduciary duty. The court concluded that plaintiffs did not have to show good cause under Rule 16 because that requirement did not apply to Rule 25(c) motions. The court noted that substitution under Rule 25(c), unlike under Rule 16, “does not alter the claims and ‘[t]he merits of the case and the disposition of the property are still determined with respect to the original parties.’” In short, “Imposing a good-cause requirement on Rule 25(c) motions is nonsensical given the purpose served by the rule. Substitution is not mandatory and, even if a party does not seek substitution, the judgment will be binding on a successor-in-interest. The Rule simply serves as a mechanism to simplify the action and expedite the ultimate resolution.” The court further ruled that even if Rule 16 applied, it would not bar plaintiffs’ motion because CapTrust did not demonstrate that it would be prejudiced by the substitution (although the court noted that plaintiffs “unduly delayed” filing their motion to add CapTrust as a party). Finally, the court addressed whether ERISA bars successor liability for claims of breach of fiduciary duty. CapTrust argued that Section 409(b) of ERISA precludes successor liability, but the court noted that courts have applied successor liability in the ERISA context, particularly for withdrawal liability and delinquent contributions. The court found that ERISA’s purpose supports applying successor liability to breaches of fiduciary duty, as it aligns with the statute’s goals of protecting employee interests. The court directed CapTrust to submit a letter identifying specific factual allegations that it contends are disputed, and for which an evidentiary hearing regarding successor liability might be necessary, by March 2, 2026.

Eighth Circuit

Meilstrup v. Standing Rock Sioux Tribe, No. 1:25-CV-162, 2026 WL 352690 (D.N.D. Feb. 9, 2026) (Judge Daniel L. Hovland). Daniel Meilstrup worked at Prairie Knights Casino in North Dakota as the Chief Executive Officer and General Manager. The casino is owned and operated by the Standing Rock Sioux Tribe. Meilstrup initiated this action to challenge the casino’s actions in mishandling his termination, which caused delays and disruptions to his wife’s medical care. He has alleged claims under ERISA and common law against the Standing Rock Sioux Tribe and related defendants. In our October 15, 2025 edition, we covered the court’s order denying defendants’ motion to dismiss as to Meilstrup’s ERISA claim, which ruled that (1) Meilstrup’s claim was properly pled, (2) defendants’ operation of a non-governmental plan waived their sovereign immunity as to the claim, and (3) the tribal court did not have jurisdiction over the claim. Now the Tribe has brought a motion to stay the proceedings while the tribal court handles non-ERISA issues relating to Meilstrup’s termination, contending that a stay is warranted under federal abstention doctrine. “Abstention is a judge-made doctrine that allows a federal court to abstain from exercising its jurisdiction when parallel state court proceedings are pending and doing so would result in the conservation of judicial resources.” The court made short work of the motion. The court noted that “a federal district court must exercise its jurisdiction over claims unless there are ‘exceptional circumstances’ for not doing so,” and “[w]here jurisdiction to hear a case exists, a federal court’s ‘obligation’ to hear and decide a case is ‘virtually unflagging.’” The court ruled that defendants could not overcome this high bar: “no exceptional circumstances in this case that warrant a stay.” The court acknowledged that defendants disagreed with its prior ruling on their motion to dismiss, but “[t]he Defendants cannot evade the Court’s prior order finding that tribal courts lack jurisdiction over ERISA claims. Any ERISA claim purportedly raised in the Tribal Court litigation does not deprive this Court of its jurisdiction, nor does it provide reason for this Court to abstain from exercising its jurisdiction while a court that lacks jurisdiction rules on the issue. A stay would be futile because the Tribal Court plainly lacks jurisdiction over Meilstrup’s ERISA claim. Any rulings from the Tribal Court pertaining to Meilstrup’s ERISA claim have no effect on this case.” Furthermore, staying the case “would cause unnecessary delay and would prejudice the Plaintiff.” As a result, the court denied defendants’ motion to stay.

Provider Claims

First Circuit

Abira Medical Laboratories, LLC v. Blue Cross Blue Shield of R.I., No. 24-CV-475-MRD-PAS, 2026 WL 353339 (D.R.I. Feb. 9, 2026) (Judge Melissa R. DuBose). As Your ERISA Watch readers know, Abira Medical Laboratories, d/b/a Genesis Diagnostics, is a medical testing business that has filed dozens of actions across the country in the last few years alleging underpayment by health insurers. In this action Genesis has alleged that it performed various testing services for patients who were insured by Blue Cross Blue Shield of Rhode Island (BCBSRI). Genesis claims that these patients assigned their insurance benefits to it, creating a contractual obligation for BCBSRI to reimburse Genesis for the services rendered. However, BCBSRI allegedly failed to respond to claims, fabricated reasons to refuse payment, and underpaid other claims, resulting in a claimed debt approaching $1.8 million. Genesis filed a complaint against BCBSRI asserting claims under ERISA and state law. BCBSRI moved to dismiss, arguing that Genesis failed to identify any specific insurance contract or provision entitling it to reimbursement. BCBSRI also contended that Genesis’ claims were barred by anti-assignment provisions in the health plans and were time-barred. Addressing Genesis’ ERISA claim first, the court ruled that it was insufficiently pleaded because Genesis did not identify any specific ERISA plan or provisions entitling it to benefits. The court acknowledged that “some courts have been sympathetic to the concern raised by [Genesis], specifically its claim that they have no access to any health plans prior to filing their Complaint.” However, the court still found Genesis’ allegations far too vague. The court noted that the complaint lacked details about the ERISA plans, such as the intended benefits, class of beneficiaries, and procedures for receiving benefits. Furthermore, the court was unconvinced by Genesis’ argument that discovery was necessary in order to obtain more detailed plan information. The court noted that Genesis received assignments of benefits “which presumably includes the right to access the patients’ plan.” Furthermore, “this Court views [Genesis’] predicament as self-inflicted because it never sought to secure the Plans from their patients upon receiving the requisitions of laboratory testing, failed to plead any attempts to retrieve Plan documents directly from BCBSRI, and refused to engage in the process outlined by this Court – designed to have the Plans produced – after BCBSRI filed its initial motion to dismiss.” As a result, the court granted BCBSRI’s motion to dismiss Genesis’ ERISA claim. The court ruled against Genesis on its state law claims as well for various reasons, and thus granted BCBSRI’s motion to dismiss in its entirety and entered judgment in its favor.

Fourth Circuit

Abira Medical Laboratories, LLC v. Anthem Health Plans of Virginia, Inc., No. 3:25CV108 (RCY), 2026 WL 281172 (E.D. Va. Feb. 3, 2026) (Judge Roderick C. Young). In our second case involving Genesis this week, it sued Anthem Health Plans of Virginia, Inc. for services it provided based on requisitions that included an assignment of benefits provision. Genesis claims that Anthem failed to pay for these services, resulting in damages approaching $3 million. In its complaint Genesis alleged four counts: (1) violation of ERISA, (2) breach of contract, (3) breach of the implied covenant of good faith and fair dealing, and (4) actual and constructive fraud. Anthem filed a motion to dismiss, which the court ruled on in this order. The court denied the motion as to Genesis’ ERISA claim, ruling that Genesis sufficiently alleged standing through valid assignments of benefits from Anthem’s insureds. The court observed, “The Fourth Circuit has not defined what constitutes a ‘valid’ assignment for purposes of assessing derivative standing; the last time it appears to have even considered the concept was in 2008.” However, the court noted that “courts within the Fourth Circuit have held that Plaintiffs generally need not plead specific language of assignment for purposes of showing derivative standing.” Based on those cases, and decisions from other circuits, the court found that the following allegations by Genesis were sufficient: “medical service providers submitted requisitions for lab services to Plaintiff,” “those requisitions contained an assignment of benefits from Defendant’s insureds to Plaintiff,” “Defendant’s insureds executed the assignment(s),” and “the assignments… specifically assigned the right of payment and the right to pursue and collect such payments to Plaintiff.” The court noted that the alternative was a “tidal wave of piecemeal litigation which would bog down courts across this country and in no way benefit the ERISA plan participants.” The court also rejected Anthem’s arguments that Genesis’ claim was too thinly pled and that it failed to plead exhaustion. The court cited the Fourth Circuit’s “high-level” approach to pleading, which “recognize[s] plaintiffs’ difficulty obtaining plan documents at the early stages of litigation,” thus justifying some level of vagueness in referring to operative plan provisions. As for exhaustion, the court noted that the Fourth Circuit “has not ruled on whether administrative exhaustion is something that must be pleaded in the first instance, as Defendant argues, or an affirmative defense with the onus of proof on the Defendant, as Plaintiff argues.” However, the court sided with the latter, “in line with the positions of the Second, Third, and Fifth Circuits,” thus ruling that Genesis did not have to plead around the exhaustion defense, and leaving the issue for another day. The court then turned to Genesis’ state law claims. It denied Anthem’s motion as to the claims for breach of contract and breach of the implied covenant of good faith and fair dealing, ruling that Genesis plausibly alleged a legally enforceable obligation, a breach of that obligation, and resulting damages. (However, the court indicated that Genesis might not be able to pursue both claims if they were factually duplicative by the summary judgment stage.) The court granted Anthem’s motion as to Genesis’ fraud claim, finding that Genesis’ “general, conclusory, and anonymous allegations regarding its course of dealing with Defendant and/or Defendant’s ‘representatives’ are insufficient to state a claim for fraud under either Virginia law or [Federal Rule of Civil Procedure 9(b)].” Finally, Anthem argued in its motion that Genesis had improperly combined 2,170 claims for services rendered to over 1,000 patients into one action. The court “appreciate[d] Defendant’s concern for its case management capabilities,” but ruled that Genesis’ claims were proper under Federal Rule of Civil Procedure 18, which gives a plaintiff the “freedom to assert as many claims as the plaintiff chooses.” The court admitted that the number of claims was “certainly a large number,” but they were still “related” and thus Genesis, as “the master of the complaint,” could combine them. Plus, “Defendant does not acknowledge the alternative to permitting Plaintiff to bring all its claims together, i.e., that the Court would be inundated with duplicative, claim-by-claim litigation.” Thus, “the Court will not sever and dismiss the claims underlying Plaintiff’s Complaint simply because Defendant is daunted by the discovery process.” As a result, Anthem’s motion was largely unsuccessful, as it was only able to eliminate one of Genesis’ claims and failed to break up the lawsuit.

Retaliation Claims

Sixth Circuit

Tascarella v. Aptiv US General Services Partnership, No. 4:26-CV-0024, 2026 WL 294962 (N.D. Ohio Feb. 4, 2026) (Judge Benita Y. Pearson). In September of 2025 defendant Aptiv US General Services Partnership (the American subdivision of a Swiss automotive technology supplier), offered Daniel Tascarella a job as the plant manager of its Ohio facility. He began work on September 29, but only worked two days before stopping due to health issues and taking a medical leave of absence. From its conversations with Tascarella, which included Tascarella informing Aptiv that he was on a liver transplant recipient list, Aptiv concluded that his absence would be lengthy and chose to terminate him as of December 31, offering him a severance agreement. On the date of his termination, Tascarella filed this action in state court alleging six claims: ERISA interference, promissory estoppel, fraud in the inducement, unilateral contract, disability discrimination, and unlawful retaliation. Tascarella also sought a temporary restraining order (TRO) and a preliminary injunction seeking the continuance of his healthcare and employment benefits. The state court initially granted an ex parte TRO, after which Aptiv removed the case to federal court. In this order the court considered Tascarella’s motion for a preliminary injunction, addressing the four required elements: “(1) the movant has a strong likelihood of success on the merits; (2) the movant would suffer irreparable injury without injunctive relief; (3) granting injunctive relief would cause substantial harm to others; and (4) the public interest would be served by granting injunctive relief.” First, the court found that Tascarella was unlikely to succeed on the merits of his ERISA retaliation claim. At the outset, it was unclear whether ERISA governed his short-term disability benefits; Aptiv contended that these benefits were a “payroll practice” exempt from ERISA. Furthermore, the court found that Tascarella was only able to show “at best, an inference of retaliation or improper termination.” The court was more persuaded by Aptiv, which contended that its decision to terminate Tascarella’s employment was based on business needs – i.e., keeping its Ohio factory operational – and not on any intent to interfere with ERISA benefits. On the “irreparable injury” prong, the court determined that Tascarella had not met his burden because he remained insured under COBRA and was eligible for Social Security and Medicare. The court noted that the benefits at risk were monetary in nature, and thus victory at trial would remedy any harms Tascarella might suffer. The court ruled that the remaining two factors also did not favor Tascarella. “Granting injunctive relief under these circumstances – absent a showing of Aptiv’s specific intent to avoid ERISA liability – would mean that ‘every employee discharged by a company with an ERISA plan would have a claim under § 510.’” Furthermore, “there are…reasons justifying employer decisions – however difficult or emotionally fraught they may be – to terminate an employee unable to perform the duties for which they were hired.” Thus, the public interest was not served by issuing an injunction. As a result, the court denied Tascarella’s motion for a preliminary injunction and the case will proceed as usual.

Statute of Limitations

Third Circuit

Hamrick v. E.I. du Pont De Nemours & Co., No. CV 23-238-JLH-LDH, 2026 WL 353624 (D. Del. Feb. 9, 2026) (Magistrate Judge Laura D. Hatcher). This case involves two class action complaints filed under ERISA against E.I. du Pont de Nemours and Company and related defendants. In one complaint plaintiffs Mary J. Hamrick, David B. Beckley, and Valentin Rodriguez contend that defendants “improperly reduced [Income-Leveling Option (“ILO”)] benefits for participants and beneficiaries below the amounts that they would receive if those benefits had been calculated using the Treasury Assumptions in violation of ERISA § 205(g).” They claim defendants used an outdated formula with a higher interest rate and an antiquated mortality table. In the second, James M. Manning contends that defendants “improperly reduced [Spouse Benefit Options (“SBOs”)] for participants and beneficiaries of the Plan below the amounts that they would receive if those benefits were actuarially equivalent to a [single life annuity (“SLA”)] in violation of ERISA § 205(d).” Again, outdated mortality tables were the alleged culprit. Defendants initially filed a motion to dismiss, contending, among other arguments, that plaintiffs’ claims were time-barred. The court denied this motion because defendants did not establish when plaintiffs’ claims accrued. According to the court, defendants did not meet their burden of demonstrating when the plaintiffs were on notice that their benefit calculations were wrong. (Your ERISA Watch covered this decision in our February 7, 2024 edition.) Defendants filed a motion for summary judgment in which they took a second swing at the timeliness argument. They argued that plaintiffs’ claims were subject to a one-year statute of limitations under 10 Del. C. § 8111; plaintiffs responded that laches, rather than a statute of limitations, should govern the timeliness of their claims. Relying on Third Circuit precedent, the court agreed that § 8111 (which governs claims for wages or salary) applied because it was the state law most analogous to plaintiffs’ claims regarding their benefits. Plaintiffs argued that they sought equitable relief, not the recovery of benefits, and that laches should apply. However, the court found that plaintiffs’ claims for increased benefits were legal in nature because they sought monetary relief. Even if the claims were equitable, laches would not exclude the statute of limitations as an affirmative defense. This left the question of when plaintiffs’ claims accrued. Defendants contended that “Plaintiffs’ claims accrued in 2019 when they made their pension elections, received documents from Defendants ‘making them aware of the material facts underlying their claims’ and, thereafter were not diligent in ensuring the accuracy of their benefit awards.” Meanwhile, plaintiffs contended that “documents they received did not amount to a ‘clear repudiation’ of their benefits and accordingly, they could not have reasonably discovered any actionable harm.” The court found this issue “a close call” and concluded that summary judgment was not warranted because there was a “genuine dispute of material fact regarding Plaintiffs’ diligence.” The court agreed with defendants that plaintiffs’ claims were repudiated when they were informed of their benefit amounts, but was not convinced the repudiations were “clear and made known” to plaintiffs because correspondence was ambiguous as to which assumptions defendants were using in calculating benefits. The magistrate judge thus recommended denying defendants’ motion for summary judgment without prejudice, allowing them to raise timeliness for a third time at trial.

Seventh Circuit

Garippo v. Skokie Valley Air Control Inc., No. 24-CV-03346, 2026 WL 296391 (N.D. Ill. Feb. 4, 2026) (Judge John Robert Blakey). Robert Garippo and Michael Garippo are former employees of Skokie Valley Air Control Inc. (SVAC) who filed this action against SVAC and their father (William Garippo) and uncle (Tony Garippo), who were executives at the company. Plaintiffs raised two disputes in their complaint. First, they contended that in 2011 Tony told them they could no longer contribute to SVAC’s retirement plan due to insufficient participants, which was untrue, as other employees continued to contribute. “No one told Plaintiffs that Tony’s statement was false or otherwise corrected this information about Plaintiffs’ eligibility to contribute to the Plan.” Second, plaintiffs contend that around 2005, Tony and William entered into a shareholders’ agreement that gave plaintiffs a right of first refusal to purchase the company if it ever went up for sale. In 2023 SVAC was purchased by another company, but plaintiffs allegedly were never informed of the offer or given an opportunity to match it. Plaintiffs alleged three claims for relief. The first was for breach of fiduciary duty under ERISA, and the other two claims relating to the sale of the company were brought under state law. Defendants moved to dismiss all three claims, contending first that plaintiffs’ ERISA claim was time-barred. The court agreed. The court explained that an ERISA claim for breach of fiduciary duty expires “six years after (A) the date of the last action which constituted a part of the breach or violation, or (B) in the case of an omission the latest date on which the fiduciary could have cured the breach or violation.” There is an exception for “fraud or concealment,” which delays the clock from starting until “the date of discovery of such breach or violation.” Here, because plaintiffs brought suit 13 years after they were allegedly told in 2011 that they could not contribute to the plan, they needed to satisfy the fraud or concealment exception. However, the court noted that this exception requires a plaintiff to show “actual concealment” or “‘steps taken by wrongdoing fiduciaries to cover their tracks.” Here, “Plaintiffs merely state that no one at SVAC told them the truth; the Complaint does not plead any fact reflecting actions of actual concealment. Without more, Plaintiffs’ allegations remain insufficient to trigger the fraud or concealment exception.” As a result, plaintiffs’ clock expired in 2017, and their ERISA claim was too late. As for plaintiffs’ state law claims, the court ruled that it did not have subject matter jurisdiction over them, and dismissed them without prejudice. Thus, defendants’ motion to dismiss was granted in its entirety and the case was terminated.